Journal of Management and Business Administration, Vol. 1, No. 1, 2016

Author: Peter R. Mutungu Mwangi

Department of Entrepreneurship and Technology, Leadership and Management, College of Human Resource Development, Jomo Kenyatta University of Agriculture and Technology

E-mail: rpmutungu@gmail.com/rpmutungu@yahoo.com

Abstract

Agency banking involves contracting of independent business entities by financial institutions to offer selected financial services to their customers. In the recent past, agency banking has attracted attention among scholars. While much literature examine the benefits of agency banking to the banks and customers, little scholarly work has focused on the agent’s perception and the actual benefits that accrue to the bank agents themselves. The main purpose of this study was to examine perception and exploitation of entrepreneurial opportunities in Agency banking in Kenya. This study employed a cross-sectional survey research design for its appropriateness in reaching out to a representative sample size. The study involved fifty Equity Bank Agents in Kiambu County. The choice of Equity agents was informed by the fact that Equity Bank led the way in implementing agency banking and its agents also do agency banking for other banks as exclusivity is prohibited by the Central Bank of Kenya guidelines. Questionnaire was used as the main data collection instruments since it facilitates self-administration, is time-saving and generates quantitative data which are coding friendly. From the analysis, the study showed that there are a number of existent opportunities in agency banking including money transfer services and multiple agency banking services and selling prepaid services such as airtime and electricity mainly due to relative ease of implementation. The key factors that determined the level of exploitation of the entrepreneurial opportunities included capital constraints and management challenges especially human resource aspect. The main risks involved in agency banking were physical risks (74%) and fraud (51%). The study recommends that the banking industry to promote agency banking through repackaging training programs that promote entrepreneurship management and skill development. The industry further needs to provide affordable capital to agents to enable them to effectively run the agency model.

Keywords: Agency banking, Agency banking entrepreneurial opportunities, Agency banking perceptions, agency banking risk factors, Equity Bank agency banking

1. Introduction

Agency banking is a banking model where financial institutions contract independent business entities to offer selected financial services to their customers on their behalf (Mas & Siedek, 2008). Kenya has pioneered agency banking with over seventeen (17) commercial banks having rolled out agency banking by end of June 2015 (CBK, 2015). The rationale of using agency banking model is to help financial institutions to divert existing customers from crowded branches providing a “complementary”, often more convenient channel. Other financial institutions, especially in developing markets, use agents to reach an “additional” client segment or geography (Ignacio, 2013). Reaching poor clients in rural areas is often prohibitively expensive for financial institutions since transaction numbers and volumes do not cover the cost of a branch (Siedek, 2008). In a nutshell the agent banking model is designed to assist banks to lower their costs of offering banking services that has been a major impediment to inclusion while at the same time improving their earnings as more Kenyans are offered an opportunity to access financial services (Wafula, 2011). Agency banking has a number of benefits not only to the Banks but also to all other stakeholders including the bank agents and the customers. Banks benefit through wider customer reach, lower fixed costs and profits; bank agents benefit through the increased revenue from transactions while customers benefit from the convenience and flexibility of the services.

Agency banking belong to Micro and Small Enterprises (MSE) sub-sector. In Kenya, the sub-sector contributed over 50% of new jobs created in 2005. Despite their significance, MSE are faced with the threat of failure with past statistics indicating that three out of every five fail within the first few months (Bowen, Morara & Mureithi, 2009). Agency banking, just like other businesses in the sub-sector, continues to face a number of hurdles and appear not to fully utilize the opportunity in agency banking.

Banks in their quest to put on board potential agents and to create more opportunities for entrepreneurs, did propose agency banking model. Surprisingly however, five years after its introduction in Kenya, a substantial number of agents have closed down the agency business. The survival of agency banking should be a major concern not only to the three main stakeholders but to all of us due to its contribution at both micro-economic and macroeconomic level. This has led to the question of whether the bank agents have identified opportunities associated with agency banking and utilized them to improve their business revenue hence their chances of survival. This study was therefore conducted to address the question of perception and exploitation of the opportunities that come with agency banking among the Kenyan banking agents.

2. Methodology

A cross-sectional survey research design was utilized owing to the vastness of the study site and the target population. The design is invaluable especially when describing the characteristics of a large population. It makes use of large samples, thus ensuring that the results are statistically representative. The design also makes use of questionnaire as the major collection tool (Owen, 2002).

The target population for this study included all agents from thirteen banks in Kenya. Agents from equity were purposively selected since the bank pioneered in agency banking in Kenya. A representative sample of sixty two (62) Equity agents, which accounted for 10% of the total population (Gay & Diehl, 1992), were selected out of 620 agents in Kiambu County using systematic random sampling technique. The technique ensured that there was no bias in the selection process.

Primary data were collected using questionnaire method from the agents. This method was found appropriate since it could reach the participants with ease. Each agent was issued with a questionnaire. The collected data were processed with the help of Ms Excel and SPSS. The findings were presented in frequencies and percentages and summarized using tables and figures.

3. Results

3.1 Background characteristics

Slightly over half (51%) of the participants were males while the remaining 49% were females. A third (66%) of them were aged between 31 and 50 years. Only 26% of them were above 50 years. Among the agents who took part in the study, 26% of them were dormant meaning they were no longer operating their agency banking business. Almost half of them demonstrated high prevalence of entrepreneurial personality traits such as risk taking, optimism, high locus of control, need for achievement and innovativeness among others as evaluated by the bank agent supervisors.

Out of a total of 35 active agents, only 3 of them had formal training in business management representing 9%. On business experience, 19 out of 35 active agents (54%) were below 5 years and the rest were above 5 years. The agency banking business was dominated by sole proprietorships and family-owned partnerships in the Micro and Small Enterprises (MSE) sector who constituted (94% of participants and mainly operated retail outlets (86%) dealing with daily consumables such as maize flour, stationery, animal feeds and airtime. Services and manufacturing industry did not appear to be keen on agency banking.

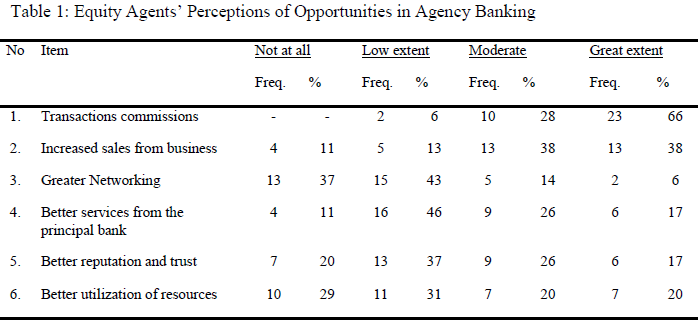

3.2 Agents’ Perceptions of Opportunities in Agency Banking

The study sought to find out the agents’ perception on entrepreneurial opportunities identified to come up with agency banking. The agents were presented with a number of hypothesized entrepreneurial opportunities of agency banking. These included transactions commissions, increased sales from business, greater networking, better services from the principal bank, better reputation and trust and better utilization of resources. Table 1 shows the distribution of the agents’ responses.

3.3 Exploitation of the Entrepreneurial Opportunities in Agency Banking

The study was interested in finding out the level, factors and risks associated with the exploitation of opportunities in agency banking.

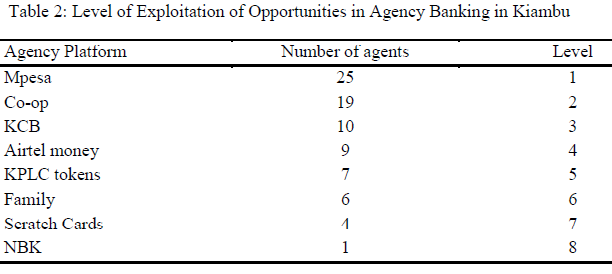

3.3.1 The Level of Exploitation of Opportunities in Agency Banking

In order to determine the level of exploitation of opportunities in various other agency banking platform (besides Equity Bank), the participants were provided with a number of banks, Mobile Money Transfer services (MTS) and prepaid services options. These included M-Pesa, Cooperative bank, KCB, Airtel Money, KPLC Tokens, Family Bank, Scratch cards, and National Bank of Kenya (NBK). Table 2 shows the distribution of the participants on the level of exploitation of agency banking opportunities.

As shown by Table 2, the most exploited agency related opportunity by Equity bank agents was M-Pesa with 25 agents. The second ranking agency platform was Coop bank with 19 agents. Other platforms had only a small number of agents. KCB had 10 agent, Airtel money had 9. The least was National Bank of Kenya (NBK) with only 1 agent in the site of the study.

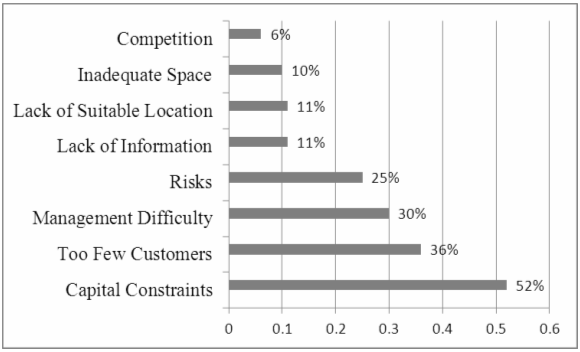

3.3.2 Factors Affecting the Exploitation in Agency Banking

The study sought to establish the major factors affecting the level exploitation of entrepreneurial opportunities in agency banking. Figure 1 shows the distribution of the participants by the factors affecting the exploitation of opportunities in Agency Banking.

Figure 1: Factors affecting the exploitation of opportunities in agency banking

The participants felt that there were a number of factors that affected the full exploitation of entrepreneurial opportunities availed to them by agency banking. Slight over half (52%) of the participants indicated that capital constraints was the main factor affecting the exploitation of opportunities in agency banking. Another 36% of them felt that too few customers was another major factor affecting the exploitation of opportunities in agency banking. Managerial difficulty was another hindering factor at 30%. Other factors included risks involved (25%), lack of information and business location (11%) respectively and lack of space (10%). Competition was the least with only 6% of the participants indicating that it was a factor affecting exploitation of opportunities in agency banking.

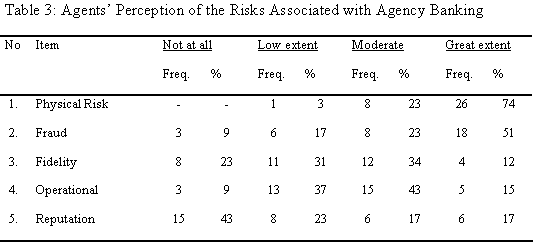

3.3.3 Risks Associated with Exploitation of Agency Banking

The study sought to find out the risks that agents thought were associated with Agency Banking. The participants were presented with a number of associated risks including physical risks, fraud, fidelity, operational and reputation risks. Table 3 shows the distribution of the agents’ responses on the perceived risks.

The physical risks of loss of money and sometimes loss of life was ranked the highest among the agents involved in the study where majority (74%) agreed that they perceived this as a risk to a great extent. Another associated risk was fraud with 51% of the participants perceiving it as a risk to a great extent.

4. Discussion

The uptake of agency banking is itself entrepreneurial and therefore requires entrepreneurial personalities to venture. The entrepreneurial process requires a cost-benefit analysis also broadly referred to as risk-return analysis to determine its worth. It was therefore observed that most agents are aware and appreciate the opportunities that bring immediate monetary benefits and fear the risks that could bring immediate financial loss. However non-monetary benefits such as improved reputation and trust and greater networking did not score highly as perceived benefits of agency banking indicating that most agents are only mindful of immediate and direct benefits of agency banking that has direct effect on cost and income. This could probably relate with the level of operation where most agents are MSEs and they mainly and regrettably do not carry out proper strategic planning in their operation (Iorun, 2014) hence short-term survival plans with key emphasis on quick monetary gains as compared to corporate entities whose strategy is long term and development of a strong brand is part of their key agenda.

The study found that agency banking was mainly dominated by family-owned MSEs and identified Money Transfer Services and Agency Banking Services from other banks as the main opportunities related to agency banking. It is also apparent from the findings that agency model mostly succeeded for the banks that had already appealed to the masses and had a strong brand presence on the ground before venturing into it. While many agency banking platforms may seem more entrepreneurial, in practice the fewer well-funded products and services were more effective than many unfunded product & services in terms of maximized returns and less management complexity.

The main factors cited as limiting exploitation of entrepreneurial opportunities related with agency were capital constraints, low returns, high risks and management challenges with a bias of staff management problems. It is worth noting that in some cases, capital constraints may not necessarily mean lack of access to capital but rather opportunity cost of capital availed to agency where the same capital may generate more revenue in another venture and therefore diverted from agency banking. The agents albeit unconsciously seem to heavily borrow from Dyer’s prioritization matrix (Dyer, 2004) where ease of implementation and relatively higher returns seemed to play a key role in deciding which banking platform or money transfer service to prioritize.

5. Conclusions

The perceptions behind seeking opportunities in agency banking are purely driven by monetary gains. Thus, if banks do not strategically position themselves to provide competitive terms in agency banking, the model is likely to experience further decline.

While there were no major hindering factors in embracing opportunities in agency banking, there appeared to be a general lack of managerial skills and financial muscles among agents for them to be able to breakeven in their business.

Competition appeared to be not a major source of risk in agency banking. Thus, agency banking appears to be not quite exciting business among entrepreneurs. This could be associated with the risk factors associated with the business which include but not limited to financial constrains, physical and frauds related risks.

Due to limitation of time and resource, the study was only able to cover Equity Agents in Kiambu county. Therefore, there is need to study the major factors related to agency banking survival and viability across all the banks that have rolled out agency banking. Agents dormancy in particular needs to be studied as it is a major indictment to an otherwise very promising model. Management skills as a driver to growth of Agency banking business also need to be studied. Other elements of agency banking that need to be reviewed are its impact on financial inclusion agenda such as access to mainstream credit.

References

Bowen, M., Morara, M., & Mureithi, S. (2009). Management of Business Challenges Among Small and Micro Enterprises in Nairobi-Kenya. KCA Journal of Business Management, 2(1).

Central Bank of Kenya [CBK] (2015). CBK Statistical Bulletin. Nairobi: CBK.

Dyer, T. (2004). Design Institute – Prototype Awards Seminar – 20 November 2004. Retrieved from http://slideplayer.com/slide/7835103/

Gay, L.R. & Diehl, P.L. (1992). Research Methods for Business and Management. New York: Macmillan.

Iorun, J. I. (2014). Evaluation of Survival Strategies of Small and Medium Enterprises in Benue State, Nigeria. International Journal of Academic Research in Accounting, Finance and Management Sciences, 4(2).

Mas, I. (2009). The Economics of Branchless Banking. Innovations, 57-59.

Mas, I., & Siedek, H. (2008). Banking Through Network of Retail Agents. (CGAP, Ed.). Focus Note, 47, 2.

Owens, L. K. (2002). Introduction to Survey Research Design. Chicago: ResearchGate.

Siedek, H. (2008). Extending Financial Services with Banking Agents. Washington DC: CGAP.

Wafula, P. (2011). New Agency Banking Deepens Access. Business Daily.