![]()

< Author: Nicholas Ngatia Njoroge, Department of Marketing and Management,

The Catholic University of Eastern Africa. P O Box 62157. 00200, Nairobi – Kenya >

Abstract

Despite that Small and Medium Enterprises sub-sector is increasingly being recognized as the prime vehicle for economic development in both developed and developing nations, there are still many SMEs that resist using strategic management practices since some of them think that this process is only useful for larger organizations. This study sought to establish the effect of strategic management practices on tax positioning among SMEs in Nairobi County, Kenya. A cross-sectional survey research design was adopted in the study. The target population of the study was all workers from 82,963 registered SMEs located in Nairobi County. A sample size of 150 respondents was used in the study. A questionnaire with close ended questions was used to collect primary data. To ensure that the instruments were valid, content validity was used. Test retest method was used to estimate reliability of instrument. Data from questionnaire were coded and entered in the computer using Statistical Package for Social Science (SPSS) Version 21. The data were then presented using frequencies and percentages and summarized using tables. Regression analysis was conducted to assess the relationship between strategic management practices use and tax positioning among small and medium enterprises. The study found that the SMEs are positioning themselves well and are adopting strategic management practices even though most of the business owners felt that strategic management was meant for big firms. The study concluded that there is a need for SMEs to embrace various strategies so as to remain relevant in the market and to strategically position themselves. Thus, it is recommended that SMEs should embrace various strategies to remain relevant in the market and to strategically position themselves. The study further recommends that the firm’s management should establish a unique operation status in dealing with varieties of business activities and should also formulate strategies to encounter business rivals and enable the firm to fulfil its business activities.

Keywords: Tax Positioning, Strategic Management Practices, Strategic Options, Tax Planning, Strategic Thinking, Ethical issues, small and medium sized enterprises

1. Introduction

Strategic decisions deal with matters that are central to the livelihood and survival of an organization or business and because of this strategic management requires a great portion of business resources (Higgins, 2005), most of which small and medium-sized enterprises (SMEs) may not have. This is because strategic decisions look for new areas of concern and issues that are unusual from the routine operational decision making. From this, a comprehensive plan is formulated to integrate the organization/business goals and the changing environment under which the business operates in. This ensures that strategic advantages of a firm are realized despite the challenge of a changing business environment (Higgins, 1986).

Adoption of superior strategic management practices provide small firms with new tools for survival, growth and maintaining a sustainable competitive advantage (Omerzel & Antoncic, 2008). SMEs use strategic planning as a tool to cushion them from the unstable business environments in order to ensure their survival and growth (Huang, 2006). Dansoh (2005) posits that strategic planning enables SMEs to be forward looking and vigilant to be able to cope with these circumstances. Small and medium enterprises, which engage in strategic planning, are more likely to be those that achieve higher sales growth, high returns on assets, higher margins on profit, higher employee growth, achieve international growth, and are less likely to fail (Wang, Walker and Redmond, 2007). Strategic planning provides an operational framework, which allows an organization to enjoy competitive advantages and improved business performance (Pillania, 2008). In order for SMEs to succeed and sustain their businesses, they need to adopt superior strategic management practices (Dansoh, 2005).

In Kenya, SMEs are a vital source of employment in the country (Republic of Kenya, 2005). This sector employs 74% of the labour force and contributes to over 18% of the country’s gross domestic product (GDP). Small enterprises in Kenya employ 1-50 employees annually and a medium size enterprise will have 50-100 employees. The Government of Kenya recognizes the impact of SMEs in poverty reduction as outlined in Republic of Kenya (1986) on Economic Management for renewed growth, Sessional Paper No.2 of 1996 on Industrial transformation to the year 2010, The Sessional Paper No. 2 of 2005 on the development of SMEs for employment and Wealth creation (Republic of Kenya, 2003, 2012). However, SMEs are falling behind great companies in adoption of strategic management practices and the benefits of strategic management tools have not fully been exploited by these firms. There is also limited empirical evidence on whether strategic management practices among the SMEs can explain their performance differences due to proper taxation position. Further, SMEs in Kenya continue to have poor performance and face stiff competition from great firms (Otieno, 2013).

Many great corporations benefit from incorporating strategic decision making in their business model. Entrepreneurs need to constantly improve their businesses in the face of changing business environments, and this can be done through strategic management. However, this remains an area which is greatly unexplored by SME’s in aligning their businesses tax position to their favour. There is a wealth of evidence on the impact of taxation on SMEs and lengthy recommendations on the need to lower taxes for SMEs and create favourable tax policies have been given (Institute of Economic Affairs, 2012; Chigbu, Eze, & Appah, 2012; Ojochogwu & Ojeka, 2012; Thiga & Muturi, 2015; Gathigia, 2001; Mungaya, Mbwambo & Tripathi, 2012; Mwangi & Nganga, 2007). However, these recommendations have not been implemented due to the risk and implications of reduced revenue to the government.

Regardless of this and by using strategic management, SMEs can achieve their business goals while at the same time ensuring optimal effectiveness with regards to their business taxation position. Using strategic management means that the SME owner or strategic manager should understand functions and processes of strategic management and know when to employ each. SMEs have been shown to be successful and tax compliant when they use strategic management. This has been achieved by the use of measures such as tax planning, which involves development and implementation of various strategies to minimize the amount of tax given for a certain period and it also involves deciding which mode of businesses to conduct to reduce tax payment (Dailey & Frederick, 1997). Effective use of strategic management is what determines whether a business survives, succeeds or fails. Thus, there is a need to explore strategic management options which SMEs can adopt, so as to remain profitable and with an effective tax position. The study therefore sought to establish the effect of strategic management practices on tax positioning among SMEs in Nairobi County.

2. Methodology

The study employed a cross-sectional survey design because it is useful in describing the characteristics of a large population, uses great samples, thus making the results statistically significant even when analyzing multiple variables. The design also allows use of questionnaire. The target population of the study was all workers from 82,963 registered SMEs located in Nairobi County (Nairobi County Council, 2014). However, the study selected legally registered firms that conformed to KRA tax compliance requirements at the time of the study and which had been in operation for a period of at least three years. A sample size of 150 respondents was selected to take part in the study. However, the study had a return rate of 118 respondents which was equivalent to 79%.

A questionnaire which comprised of close ended questions was used to collect primary data from the study participants. To ensure that the instruments were valid, content validity was used. Test retest method was used to estimate reliability of instrument. Data from questionnaire were coded and entered in the computer using Statistical Package for Social Science (SPSS) Version 21.

The data were then presented into frequencies and percentages and summarized into tables. Regression analysis was conducted to assess the relationship between strategic management practices use and tax positioning among small and medium-sized enterprises (SMEs) in Kenya.

3. Results

3.1 Background Information

The preliminary information gathered regarding the characteristics of the respondents included: gender, level of education, and the years of employment in the organization. The study findings showed that majority (63%) of the respondents were male and the remaining 37% were female. With regard to the level of education, a third (33%) of the respondents had attained university or post graduate level, over half, 52%, of them had college qualifications and the remaining 15% of them had either certificates or secondary qualification. The respondents were asked to indicate the number of years they have been with the institution; over half gory of them (53%) had worked for a period of more than 5 years and 47% had worked for a period between 3 to 5 years.

3.2 Influence of Strategic Management Options for SMEs on Tax Positioning

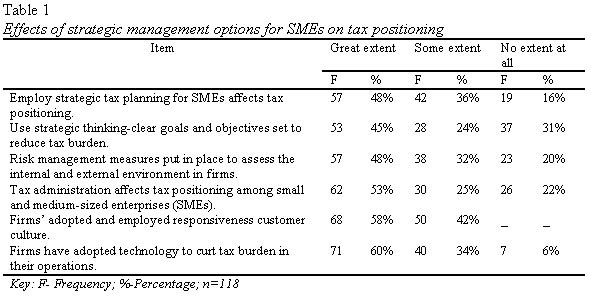

The study sought to establish strategic management options for tax burden positioning of SMEs in Nairobi County. Table 1 shows the distribution of responses against the items.

As shown in Table 1, the study findings indicated that nearly half (48%) of the respondents reported that employment of strategic tax planning influences tax positioning to a great extent, over a third (36%) of them indicated to some extent and the remaining 16% said to no extent at all. In addition, 45% of the respondents indicated that use strategic thinking-clear goals and objectives set to reduce tax burden and costs influences tax positioning to a great extent, 24% of them indicated to some extent and the remaining 31% of them reported to no extent at all. Further, nearly half (48%) of the respondents reported that risk management measures put in place to assess the internal and external environment in firms affect tax positioning to a great extent, nearly a third (32%) of them indicated to some extent and another 20% indicated to no extent at all.

With regard to whether tax administration affects tax positioning among small and medium-sized enterprises (SMEs), slightly more than half (53%) of the respondents indicated to a great extent, 25% of them pointed out that it does to some extent and the remaining 22% of them indicated to no extent at all. On whether the firm’s adopted and employed responsiveness customer culture affects tax positioning, more than half (58%) of the respondents said to a great extent and the remaining 42% of them reported to some extent. Another 60% of the respondents were affirmative that adopted technology in firms to curt tax burden in their operations influences tax positioning to a great extent. The rating by another 36% of them responded “to some extent” and the remaining 6% of them indicated to no extent at all. Thus, this implies that strategic management options for SMEs affect tax positioning in business firms.

3.3 Regression Analysis

In order to analyze the effect of strategic management practices on tax position, multiple regression analysis were computed. The five effects of strategic management practices; strategic tax planning, strategic thinking, risk management, tax administration and ethical issues were fixed as independent variables and tax positioning was set as the dependent variable.

3.3.1 Correlations

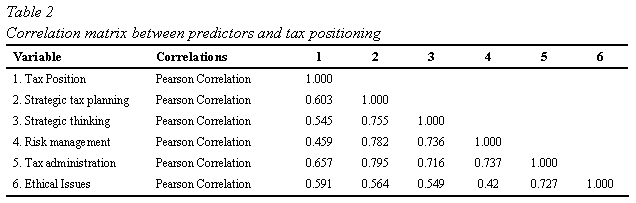

The study further investigated the effect of strategic management practices on tax position of SMEs in Nairobi County. Correlations were used to show the strength of association between strategic practices and tax position of SMEs as illustrated in table 2.

As shown in Table 2, correlation results indicated that strategic tax planning and tax positioning were strongly positively correlated with a correlation coefficient (r) of 0.603. This implies that an increase in strategic tax planning effectiveness would result in improved organizational performance and thus reduced tax burden on the business.

The results also indicated that there exists a strong, positive correlation between strategic thinking and tax positioning (r=0.545). The correlation between the variables indicates that an increase in strategic thinking in the organizations would result in improved competitiveness and this would be associated with an improvement in their profitability as indicated by a positive correlation between the two variables. This will then be translated to reduced tax burden of the SMEs.

Further, there was a moderate, positive and significant relationship between risk management and tax positioning (r=0.459). The correlation between the variables indicates that an increase in risk management mitigation strategies effectiveness in the organization would result in improved profitability and this would be associated with an improvement in their tax burden position.

In addition, tax administration and tax positioning were strongly positively correlated (r=0.657). This implies that an increase in tax administration effectiveness in the organization would be associated with an improvement in their tax burden position. Thus the SMEs have more knowledge on tax administration issues and they are better positioned on how to handle such matters.

Ethical issues and tax positioning were also found to be strongly positively correlated (r=0.591). Thus, an increase in ethical issues effectiveness in the organization would be associated with an improvement in their tax burden positioning which is an implication that for the SMEs to position themselves efficiently they have to address all the ethical issues and promote transparency and accountability.

3.3.2 R-Squared

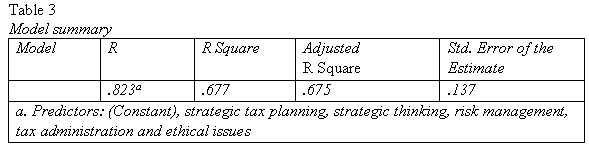

In order to determine how well the predictors (strategic tax planning, strategic thinking, risk management, tax administration and ethical issues) explained the dependent variable (Tax positioning), R computations were carried out. Table 3 shows the R squared results.

From Table 3, an R square of 0.677 indicates that 67.7% of the variations in tax positioning is jointly accounted for by the variations in strategic tax planning, strategic thinking, risk management, tax administration and ethical issues. The correlation coefficient (r) of .823 indicates that the combined effect of the predictor variables has a strong and positive correlation with tax positioning. This also meant that a change in the drivers of tax positioning (strategic tax planning, strategic thinking, risk management, tax administration and ethical issues) has a strong and a positive effect on tax positioning.

3.3.3 Regression Coefficients

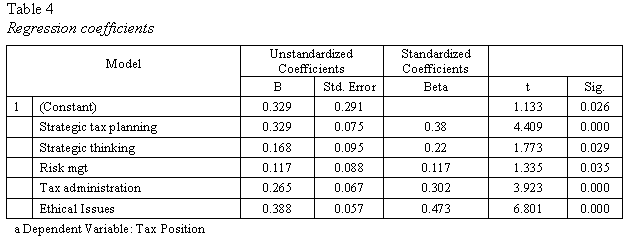

In order to determine the relative importance of the predictors (strategic tax planning, strategic thinking, risk management, tax administration and ethical issues) in predicting tax positioning, regression model equation was computed. Parameter estimates (coefficients) are shown by Table 4.

Table 4 displays the regression coefficients of the independent variables. Based on the results, the coefficient associated with the regression constant (β0) was .239 with a standard error of 0.291. In addition, strategic tax planning was statistically significant in explaining tax position of SMEs (β1=0.329, p<.001), strategic thinking and tax positioning had also a significant relationship (β2=0.168, p< .029), risk management and tax positioning had a significant relationship (β3=0.117, p= 0.035), tax administration and tax positioning had a significant relationship (β4=0.265, p<.001), while ethical issues and tax positioning had also a significant relationship (β5=0.388, p<.001). According to the analysis result, the multiple regression formula is expressed as follows:

Y’(Tax positioning) = 0.329+ 0.329 Strategic tax planning + 0.168 Strategic thinking+ 0.117 Risk management + 0.265 Tax administration + 0.388 Ethical issues + ε

The findings implies that improved strategic tax planning effectiveness by one unit leads to improved tax positioning at a rate of 0.329%; one additional unit in strategic thinking effectiveness was associated with 0.168% increase in tax positioning; one additional unit in risk management effectiveness was associated with 0.117% increase in tax positioning; one additional unit in tax administration effectiveness was associated with 0.265% increase in tax positioning; and one additional unit in ethical issues effectiveness was associated with 0.388% increase in tax positioning. Therefore, an additional unit in any of the predictors (strategic tax planning, strategic thinking, risk management, tax administration or ethical issues) would lead to an increase in the dependent variable (tax positioning) by the respective percentages as far as other variables are kept constant (e.g. one additional unit in strategic tax planning leads to improved tax positioning at a rate of 0.329% assuming that all the other variables are kept constant).

4. Discussion

The first objective of the study was to establish the strategic management options for tax burden positioning of SMEs in Nairobi County. The study findings indicated that there were various strategic options adopted by SMEs for tax burden positioning which included strategic tax planning, strategic thinking, risk management, tax administration and ethical issues. The findings imply that use of strategic management practices greatly reduces the tax burden and consequently encourages businesses to be tax compliant which increases available revenue for the county operations to create a good business environment for SMEs.

The study findings were consistent with those of Clayton (2016) who observed that strategic management is a continuous process that involves the evaluation of the businesses and industries that the organization is involved with and also appraises the goals to meet all the present and future objectives of the company while reassessing each strategy. Further, Clayton suggested that strategic thinking is most important for upper management first then the processes and strategies are later communicated to others within the organization. Once everyone in the business understands the strategy well, only then will the strategic management process will be best implemented.

The second objective of the study was to investigate the effect of strategic management practices on tax position of SMEs in Nairobi County. The findings indicated that strategic management practices influenced tax position of SMEs. This was supported by the inferential statistics computed from coded data of the respondents that shows a strong positive and significant association between strategic management practices and tax positioning of SMEs. This implies that tax burdens are reduced from the increased use of strategic management in business which encourages SMEs to be tax compliant. The correlation results indicated that there was a positive and significant relationship between tax position and strategic management practices. Correlation results indicated that tax positioning and strategic tax planning had a strong and significant positive relationship.

The study findings are in agreement with a study that was conducted by Raduan, Jegak, Haslinda and Alimin (2009) that found, strategic tax planning is important to keep a business successful and to sustain it in the long run and this can be ensured through attaining a competitive advantage through improved operational efficiencies and manipulation of factors to the advantage of the business.

Results further indicated that risk management and tax positioning were moderately positively correlated (r=0.459. This finding was consistent with a study that was carried out by Higgins (2004) that found, risk management can be done by assessing the implications of various factors on a business. These factors include: political and legal factors such as legislation on trade, tax or employment affect business while economic factors affect interest rates, economies of scale, inflation, disposable income and money supply. Overall the correlation results indicated that there was a strong positive correlation between strategic management practices (strategic tax planning, strategic thinking, risk management, tax administration and ethical issues) and tax positioning of SMEs. The findings are in support of Nyariki (2013) who investigated the role of strategic management for SME growth in Kenya and concluded that strategic management has a positive relationship with competitive advantage for a business.

5. Conclusion

The study concludes that the SMEs had adopted various strategies to position themselves in the turbulent environment and thus reduction of tax burden hence improved performance. Most of the firms agreed to a great extent that they had adopted strategies such as tax planning, environmental scanning and analysis, human resource training and development strategy, strategy formulation in line with vision and mission statements, customer care service satisfaction, and monitoring and evaluation of results.

Based on the findings, there is a need for SMEs to embrace various strategies so as to remain relevant in the market and to strategically position themselves. In addition, firm’s management should establish a unique operation status in dealing with varieties of business activities and as well formulate strategies to encounter business rivals in order to enable the firm to fulfill its business activities.

Adoption of strategic management practice is considered indispensable in small scale enterprises more especially in developing economies like Kenya. This should form part of the SMEs method of improving organizational performance to enable them cope with the changes and challenges of the unstable business environment and the global economy. Additionally, SMEs in Kenya need a good balance between the organization’s culture and the organization’s processes so as to enhance competitive advantage. This enables employees to offer customers better services, they are willing to take the time to solve difficult problems, their work is of higher quality, and they are more likely to stay with the organization.

References

Aliaga, M. & Gunderson, B. (2000). Interactive statistics. Chicago: Prentice Hall.

Chigbu, E., Eze, L. A., & Appah, E. (2012). An Empirical Study on the Causality between Economic Growth and Taxation in Nigeria. Current Research Journal of Economic Theory, 4 (2).

Dailey, C., & Frederick, W. (1997). Tax Savvy for Small Business. Berkeley, CA: Nolo Press.

Edinburgh Group, (2012). Growing the Global Economy through SMEs. Edinburgh: Edinburgh Group Research.

Feilzer, M. (2010). Doing Mixed Methods Research Pragmatically: Implications for the Rediscovery of Pragmatism as a Research Paradigm. Journal of Mixed Methods Research, 4(2), 6-16.

Gathigia, J. (2001). The Effect of Taxation on the Growth of SMEs: A Study of Small and Medium Plastic Manufacturing Enterprises in Nairobi Province, Kenya. Nairobi: Pauline’s Press.

Higgins, J. (2005). The Eight ‘S’s of Successful Strategy Execution. Journal of Change Management, 4(3), 3-13.

Higgins, J. (1986). Strategic Management and Organizational Policy. Hinsdalle, Illinois: Dryden Press.

Jofre, S. (2011). Strategic Management: The Theory and Practice of Strategy in (Business) Organizations. Denmark: Denmark Technical University.

Kamar, I. K. (2015). Effects of Government Taxation Policy on Sales Revenue of SME in Uasin Gishu County, Kenya. International Journal of Business and Management Invention, 5(4), 29-40.

Lobontiu, G.. (2002). Strategies and Strategic Management in Small Business. Copenhagen: Copenhagen Business School.

Mungaya, M., Mbwambo, A., & Tripathi, S. (2012). Study of Tax System Impact on the Growth of Small and Medium Enterprises. International Journal of Management and Business Studies, 2(3).

Mwangi, M. J., & Nganga, D. (2007). Taxation and SME’s Sector Growth. Asian Journal of Business and Management Sciences, 2(3).

Nyariki, R. (2013). Strategic Management Practices as a Competitive Tool in Enhancing Performance of Small and Medium Enterprises in Kenya. Nairobi: Government Press.

Ojochogwu, W., & Ojeka, S. (2012). Factors that Affect Tax Compliance among Small and Medium Enterprises (SMEs) in North Central Nigeria. International Journal of Business Managment, 7(12), 87-96.

Olawale, F., & Garwe, D. (2010). Obstacles to the Growth of New SMEs in South Africa: A Principal Component Analysis Approach. African Journal of Business Management, 6(2), 729-738.

Raduan, C., Jegak, U., Haslinda, A., & Alimin, I. (2009). Management, Strategic Management Theories and the Linkage with Organizational Competitive Advantage from the Resource-Based View. European Journal of Social Sciences, 11(3), 1-16.

Republic of Kenya, (2012). Economic Survey. Nairobi: Government Printers.

Republic of Kenya, (2005). Development of Micro and Small Enterprises for Employment and Wealth Creation, Sessional Paper No. 2. Nairobi: Government Press.

Saleh, A. (2012). Exploring Strategies for Small and Medium Enterprises in Saudi Arabia. Manchester: RIBM Doctoral Symposium.

Shah, A., Ahmadani, M., Shaikh, N., & Shaikh, F. (2012). Impact of Analysis of SMEs Sector in Economic Development of Pakistan: A Case of Sindh. Journal of Asian Business Strategy, 7(3), 44-53.

Stanworth, M., & Curran, J. (1976). Growth and the Small Firm: An Alternative View. Journal of Management Studies, 13 (2), 95-110.

Tashakkori, A., & Teddlie, C. (2003). Handbook of Mixed Methods in Social and Behavioral Research. Thousand Oaks, CA: Sage.

Thiga, N., & Muturi, W. (2015). Factors that Influence Compliance with Tax Laws among Small and Medium Enterprises in Kenya. International Journal of Scientific and Research Publications, 5 (6),1-12.

Zacharakis, A., Neck, H., Hygrave, W., Cox, L. (2002). Global entrepreneurship monitor. Wellesley, MA: Babson College.

Suggested Citation:

Njoroge, N.N. (2017). Effect of Strategic Management Practices Use on Tax Positioning among Small and Medium Enterprises in Nairobi County. Journal of Management and Business Administration, 2(1). Retrieved from http://writersbureau.net/journals/jmba/effect-of-strategic-management-practices-use-on-tax-positioning-among-small-and-medium-enterprises-in-nairobi-county.pdf