Journal of Management and Business Administration, Vol. 1, No. 1, 2016

Authors: Joyce Ngotho1 and Francis Kerongo2

1. Department of Commerce and Economics, School of Human Resource Development, Jomo Kenyatta University of Agriculture and Technology | E-mail: joyce.ngotho@googlemail.com

2. Lecturer, Jomo Kenyatta University of Agriculture and Technology

Abstract:

Revenue collection is very important for every government in the world as it enables the government to acquire assets which are not liable to debt and which the government uses to develop its economy. However, revenue collection in the developing economies like Kenya has not always been as effective as it should be. The ineffectiveness is attributable to many factors. This study sought to examine the determinants of revenue collection in Kenya. The study employed a case study research design since only one institution was involved in the study. A questionnaire was used for data collection. The study targeted senior and middle management staff working in the case tax institution. A total of one hundred (100) respondents formed the sample out of who 82 responded to the questionnaire. Data analysis was carried out using descriptive statistics. The findings showed that compliance levels and tax rates were factors that mainly affected revenue collection from an administrative perspective. Inflation and foreign direct investment influenced revenue collection though to some extent were beyond administrative control due to varying market forces. The study recommends the government to initiate tax compliance campaigns to sensitize citizens on the importance of tax to the life and self-sustenance of a nation.

Keywords: inflation, tax compliance, tax rates, foreign direct investment, revenue collection challenges, Kenya tax non-compliance, determinants of revenue growth, tax revenue

1. Introduction

Tax is the charge levied by the government of a country upon its habitants for its support or for the purpose of facilitating the service delivery in a country (Aamir, Qayyum, Nasir, Hussain, Khan & Butt, 2011). It is neither a voluntary payment by the tax payer nor like a donation. Rather it is an enforced payment to the government (Garner, 1999). Though the major aim of revenue collection for most governments is to stimulate and guide the economic and social development of the country, there are several determinants for an effective realization of the exercise. The obvious challenges facing revenue collection can be generalized for most countries (Garner, 1999).

For most developing countries, taxation goes hand-in-hand with economic growth and taxes are lifeblood for governments to deliver essential services and to make long-term investments in public goods (Organization for Economic Co-Operation and Development [OECD], 2008).

Over time, Kenya has moved from being a low tax burden country to a high tax burden country yet the country faces the obvious need for more tax revenues to maintain public services (KRA, 2004). The central role played by taxes has led to a number of studies being undertaken in the field of revenue collection (Wawire, 2000; Muriithi and Moyi, 2003; Wawire, 2003). Since revenue collection in Kenya has not always been as effective as it should be despite a number of studies, this study was therefore undertaken in view of examining the influence of inflation, the influence of compliance level, effect of tax rates and foreign direct investment on revenue collection in Kenya.

2. Methodology

The study employed a case study research design since only one institution was involved in the study. The design was found appropriate since it allows for use of both qualitative and quantitative approaches although it is mainly descriptive (Anastas, 1999). The study mainly relied on quantitative approach but qualitative was also sparingly used to present qualitative data from open ended items.

The study targeted senior and middle management who were considered to have relevant information on the determinants of revenue collection in Kenya. The sample frame used in this study included senior and middle level management officials. Random sampling was used to arrive at the sample size. By applying random sampling procedure, 80 middle managers and 20 senior level managers were sampled. In total, there were 100 respondents out of whom, 82 responded to the questionnaire.

Questionnaires were used to collect data from the senior level and middle level managers from the revenue collection body in Kenya. Questionnaires were found appropriate for a large population as they involve the respondents responding to the questions themselves and they are precise and time saving (Kendall, 2008). The quantitative data collected through questionnaires were analyzed with the help of SPSS and results presented in frequencies and percentages.

3. Results

3.1 Demographic Characteristics

Among the respondents, 56% were males and 44% of them were females. Evaluating the work experience of the respondents, the study established that 36% of them had worked for a period ranging between 4-7 years, 34% had worked for 7 years and above. Work experience was found to be valuable in providing relevant information on the determinants of revenue collection.

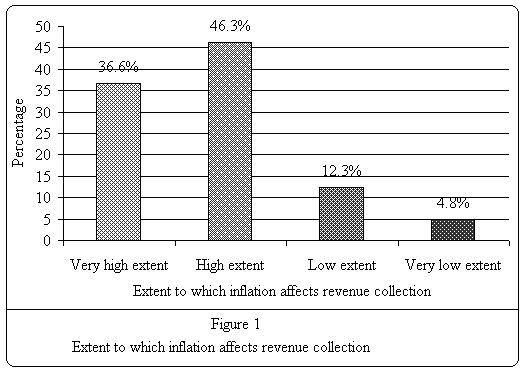

3.2 Extent to Which Inflation Level Affects Revenue Collection

The study investigated the influence of inflation on revenue collection. Figure 1 shows the extent to which inflation influenced revenue collection at the revenue collection body in Kenya

The extent to which inflation level affects revenue collection was respectively affirmed by 36.6% and 46.3% of the respondents who took part in the study. A small percentage of the respondents (4.8%) did indicate that inflation influenced only to a very low extent.

Most of the respondents further reported that when inflation rises there is a negative effect on revenue collection. In their observation the respondents indicated that when inflation falls, revenue collection increases. The inflation rise which affects the cost of living and also of doing business leads to tax evasion.

3.3 Extent to Which Compliance Level Affects Revenue Collection

The study also sought to establish the extent to which compliance level affected revenue collection and how adequately the revenue collection body had equipped itself in ensuring compliance with revenue collection. In determining the extent to which compliance level affected revenue collection in the institution, the majority of respondents, 57.4% indicated that compliance level affected tax collection to a large extent. Slightly over a third, 34.1% of the respondents indicated that it did affect to some extent. The remaining, 8.5% indicated that it did not affect as such.

When further queried whether revenue collection body was adequately equipped in ensuring compliance level, the respondents noted that the revenue collection body was not well equipped to ensure high compliance levels.

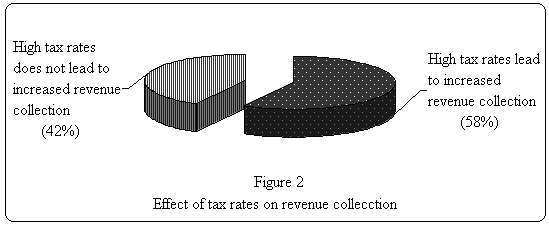

3.4 Effect of Tax Rate on Revenue Collection

From the reviewed studies, tax rates have been established as crucial determinants in revenue collection. Tax rates can encourage compliance or tax evasion. This study examined the effect of tax rate on revenue collection in Kenya.

As shown by Figure 2, a majority of the respondents, 58% agreed with the statements that high tax rates led to increased revenue collection. However, there were a considerable percentage of the respondents, 42% who felt that high tax rate did not lead to increased revenue collection by the revenue collection body. When the respondents were further asked to explain why they felt that high tax rates can lead to decreased revenue collection, they observed that increasing tax rates can lead to tax evasion which in return has an effect on the amount of revenue collected.

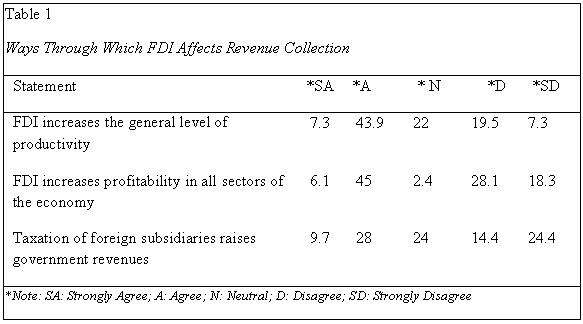

3.5 Whether Foreign Direct Investment Affects Revenue Collection

Most governments encourage foreign direct investment (FDI) placing hope on its benefits in growing the economy. The presence of FDI therefore is source of revenue in various ways to the country. This study examined whether FDI affects revenue collection. Table 1 is a presentation of the ways in which FDI affects revenue collection.

The majority of the respondents, 51.1% strongly agreed and agreed that FDI increases the general level of productivity; another similar percentage strongly agreed and agreed that FDI increases profitability in all sectors of the economy. Concerning whether taxation of foreign subsidiaries raises government revenues, slightly over a third of the respondents, 37.7% strongly agreed and agreed with the statement. However, 38.8% differed with the statement.

3.6 Interventions for Effective Revenue Collection

The study gathered various suggestions that could act as interventions for effective revenue collection.

To ensure that inflation does not affect revenue collection in a negative way, respondents suggested the following: controlling interest rates, subsidizing basic needs like food and medication, and adjusting tax rates to the prevailing inflation conditions.

The measures that were suggested to ensure sustained compliance levels included increased compliance checks, simplifying tax administration, providing education support to tax payers, moderating tax rates, improved service delivery by Kenya’s revenue collection body and reduction in corruption level.

To facilitate FDI which would positively influence revenue collection, the respondents were for the view that several areas or issues needed to be addressed. These included proper tax incentive structures, stable policies to encourage FDI, tightening compliance laws, identifying the key sectors to invest in to spur economic development, the government to improve infrastructure to attract foreign investors and the establishment of specific laws to govern foreign investors in tax compliance issues.

4. Discussion

The theorized determinants that were examined in this study included inflation, compliance level, tax rates and foreign direct investment. These factors have been examined elsewhere and most of the results have shown that they, among others, do determine revenue collection success. A study carried out in Pakistan by Rasheed (2006) observed that inflation ties up money that could be used to pay taxes by individuals and firms. Further, when inflation rises, there is an increase in tax evasion. However, according to the study, applying econometric techniques for estimating tax elasticity, inflation cannot be categorically related to tax evasion although it has an effect.

This study found that compliance level affects collection of revenue by the revenue collection body. Non-compliance to remission of taxes has been found to be a key determinant of revenue collection. An earlier study by Kiprotich, Momanyi and Nyandusi (2012) showed that Kenya is among many developing countries struggling with the problem of tax non-compliance by the tax payers. From a cross comparative analysis of previous studies and the findings of this study, it is evident that tax non compliance among business firms does affect revenue collection negatively.

According to 42% of the respondents in this study, high tax does not essentially lead to increased revenue collection by the revenue collection body. Tax rates generally scare businesses and in some cases influence the purchasing trends of the people. Therefore, by increasing tax rates, there is no given certainty that there will be more revenue generation. Where taxes are not evadable, some businesses for instance the foreign investors opt to pull out and this has a direct effect on revenue collection. Some studies recommend broadening of tax network instead of raising tax rates to the expense of affecting economic activities (Ballard, Fullerton, Shoven & Whalley, 2003).

A study by Hunay and Skudar (2006) attributed a partial contribution of economic growth to Foreign direct investment because foreign affiliates increased the general level of productivity, export propensity and profitability in all sectors of the economy. In this study, 43% and 37% felt that FDI increases the general level of productivity and therefore taxation of foreign subsidiaries raises government revenues.

5. Conclusion and Recommendations

5.1 Conclusion

Inflation rise was found to have a negative than positive effect on revenue collection due to decreased economic activities. Inflation increase directly influences the spending behavior of the people, affects the cost of doing business and therefore it should be monitored in order to ensure an effective revenue collection.

There are no proper policy provisions and mechanisms that have been implemented to ensure full tax compliance by the tax collection body in Kenya. There is need therefore to adequately equip the institution to be able to carry out its mandate.

High tax rates do not necessarily increase tax collection but can likely lead to tax evasion.

The study established that FDI increases the general level of productivity and profitability in all sectors of the economy. Thus, an investment environment that encourages FDI is positive since it enhances revenue collection.

In general, the study concluded that inflation, compliance level, tax rates and foreign direct investment to a large extent affect revenue collection in Kenya. Thus, study justifies the need for action if revenue collection performance is to be improved and sustained in Kenya.

5.2 Recommendations

The body responsible for tax collection in Kenya should come up with tax controlling systems to ensure a fixed exchange rate to prevent depreciation of the domestic currency against other major currencies. Such measures would help control inflation levels.

Concerning compliance, the study recommends that the government of Kenya should conduct tax compliance drives in order enhance service delivery to the general public through increased revenue collection. It is however, the initiative of the government to ensure the existing laws are observed and tax evaders punished.

On the basis of the tax rates, the study recommends that the government should lower the tax rates to increase voluntary compliance by tax payers since they do not feel over-burdened by taxes. This will, in return, encourage foreign direct investment.

The study further recommends that there should be incentives to encourage FDI through loosening some restricting investment policies and encourage best global investment practices.

Areas of Further Research

The study found that compliance was a major issue in Kenya. The study therefore recommends that further studies be carried out on the factors that lead to tax non-compliance in Kenya.

The study was also carried out in the context of the Kenya Revenue Authority; bearing in mind that tax collection has been customized in the East African Countries, the study recommends that further studies be carried out on challenges facing revenue collection bodies with reference to East Africa Community (EAC).

References

Aamir, M., Qayyum, A., Nasir A., Hussain, S., Khan, K.I & Butt, S. (2011). Determinants of tax revenue: A comparative study of direct taxes and indirect taxes of Pakistan and India. International Journal of Business and Social Science, 2(19) 173- 177.

Anastas, J.W. (1999). Research design for social work and the human services. Chapter 5, Flexible Methods: Descriptive Research. New York: Columbia University Press.

Ballard, C., Fullerton, D., Shoven, J.B. & Whalley, J. (2003). The Relationship between tax rates and government revenue. Chicago: University of Chicago Press.

Garner B.A. (ed.) (1999). Black’s Law Dictionary 7th Edition. West Group.

Kendall, L. (2008). The Conduct of qualitative interview: Research questions, methodological issues, and researching online. In J. Coiro, M. Knobel, C., Handbook of Research on new literacy. New York: Lawrence Erlbanm Associates.

Kiprotich, N.I., Momanyi, G. & Nyandusi, O.M. (2012). Tax administration. International Multidisciplinary Journal, 6 (1).

Kenya Revenue Authority [KRA] (2004). Staff quarterly newsletter. Retrieved from http://www.revenue.go.ke/pdf/publications/krarevnews.pdf

Muriithi, M.K. & Moyi, E. D. (2003). Tax reforms and revenue mobilization in Kenya, AERC Research Paper 131, Nairobi: AERC.

Organization for Economic Co-Operation and Development [OECD] (2008). Tax Effects on Foreign Direct Investment – Recent Evidence and Policy Analysis, OECD Tax Policy Studies No. 17. Organization For Economic Co-Operation And Development.

Rasheed, F. (2006). An analysis of the tax buoyancy rates in Pakistan. Journal of Market Forces, (3) 6.

Wawire, N. H. W. (2003). Trends in Kenya’s tax ratios and tax effort indices, and their implication for future tax Reforms in Illieva. Egerton Journal, 4,256 – 279.

Wawire, N. H. W. (2000). Revenue productivity implications of Kenya’s tax system in Kwaa Prah, K. and A. G. M. Ahmed (Ed.). Africa in transformation. Political and Economic Issues. Vol. 1 Chapter 6. Addis Ababa: OSSREA, 99 – 106.